In the rapidly evolving landscape of global finance, the definition of “transparent reporting” is undergoing its most significant transformation in decades. For years, financial performance and sustainability efforts existed in separate silos—one audited and regulated, the other often relegated to voluntary “ESG” brochures.

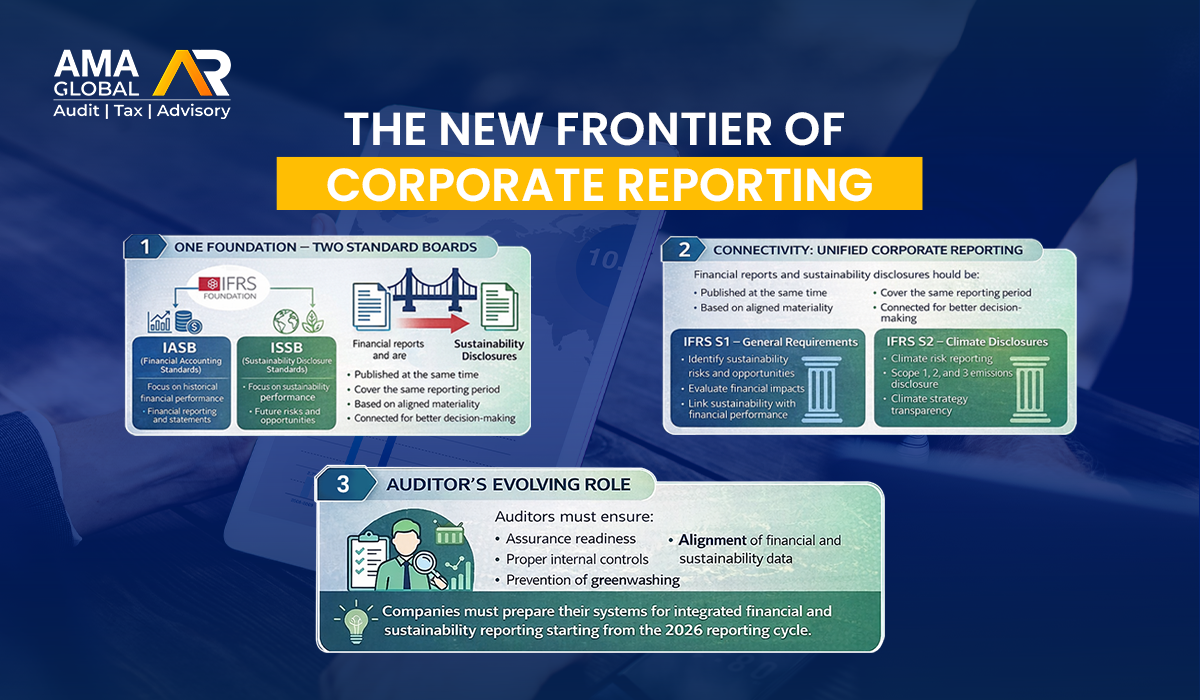

That era has officially ended. With the establishment of the International Sustainability Standards Board (ISSB) under the IFRS Foundation, we are moving toward a unified global baseline that treats sustainability data with the same rigor as financial data.

Why This Matters Now

The introduction of IFRS S1 (General Requirements) and IFRS S2 (Climate-related Disclosures) represents a shift from “compliance-driven” ESG to “value-driven” reporting. Investors are no longer just looking at profit margins; they are analyzing how climate risks, resource scarcity, and social governance impact a company’s long-term enterprise value.

The Two New Pillars of Disclosure

- IFRS S1: The Framework for Connectivity

IFRS S1 requires companies to disclose information about all sustainability-related risks and opportunities that could reasonably affect their cash flows, access to finance, or cost of capital. It demands that sustainability disclosures be published alongside financial statements, ensuring a “joined-up” view of the business.

- IFRS S2: The Climate Mandate

This standard specifically addresses climate-related risks. It requires detailed disclosures on physical risks (like the impact of extreme weather on supply chains) and transition risks (like the cost of moving to a low-carbon economy). Crucially, it mandates the reporting of Scope 1, 2, and 3 greenhouse gas emissions, providing a transparent look at a company’s entire carbon footprint.

The Auditor’s Perspective: Beyond the Balance Sheet

As auditors, this transition brings new responsibilities and challenges. The integration of these standards means that sustainability data must now be investor-grade. This requires:

- Robust Internal Controls: Companies must implement systems to capture sustainability data that are just as reliable as their accounting software.

- Materiality Alignment: There must be consistency across reports. If a company identifies a significant climate risk under IFRS S2, auditors will look for its reflection in the financial statements—such as asset impairments or changes in the useful life of machinery.

- Verification and Trust: Bringing this data into the primary financial report reduces the risk of “greenwashing” and builds essential trust with stakeholders and regulators.

Preparing for the 2026 Reporting Cycle

The transition period is narrowing. For firms operating in the UAE and globally, the time to evaluate reporting systems is now. Moving toward the 2026 cycle, businesses must ensure their finance and sustainability teams are no longer working in isolation but are collaborating to tell a single, cohesive story of value creation.

Is your organization ready for the convergence of financial and sustainability reporting? Connect with our audit team today to discuss your transition strategy.

Monish Mohan is a versatile and accomplished Auditor, VAT Consultant, Finance and Accounts Professional offering over 18 years of experience in UAE VAT, Audit & Assurance, Finance management Advisory & Accounting & bookkeeping.